As of 2026, the amount of CPF Ordinary Account (OA) savings you can use for housing depends primarily on the property's remaining lease:

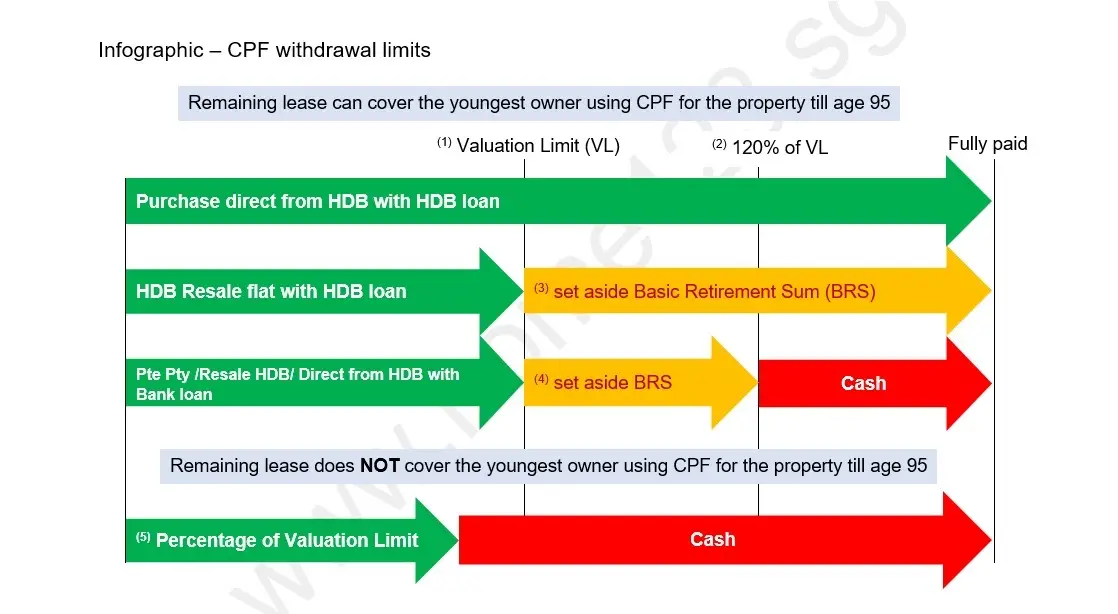

The infographic presented is for buyers who do not have any existing property financed with CPF Ordinary Account (OA) savings.

Valuation Limit (VL): The lower of the purchase price or the valuation of the property at the time of the purchase.

Withdrawal Limit (WL): Capped at 120% of the Valuation Limit.

| Property Type | Financing Method | CPF amount to set aside | CPF OA usage |

|---|---|---|---|

| Direct flat from HDB | HDB loan | NIL | Fully pay your HDB loan using CPF OA |

| Resale HDB Flat | HDB loan | Basic Retirement Sum (BRS) | Up to the Valuation Limit (VL). After setting aside the BRS, you may continue using your CPF OA |

| Private property / HDB resale / Direct flat from HDB | Bank loan | Basic Retirement Sum (BRS) | Up to the Withdrawal Limit (WL), after which no further usage is allowed. |

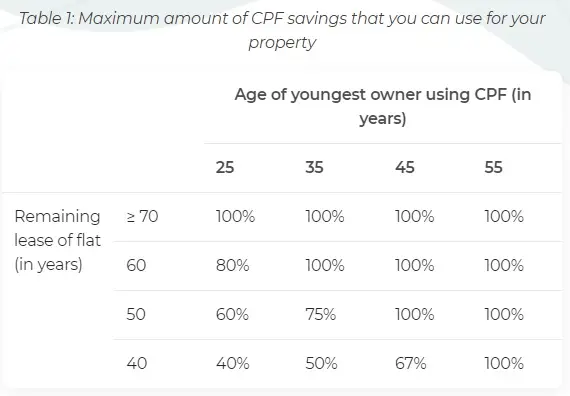

CPF OA can be used up to a percentage of the Valuation Limit (VL).

Table 1 shows the percentage of Valuation Limit based on the remaining lease of the property at the time of purchase.

Example of percentage of Valuation Limit:

Younger buyer age: 35

Remaining lease: 50 years

Maximum amount of CPF can be use: 75% of the Valuation Limit (VL)

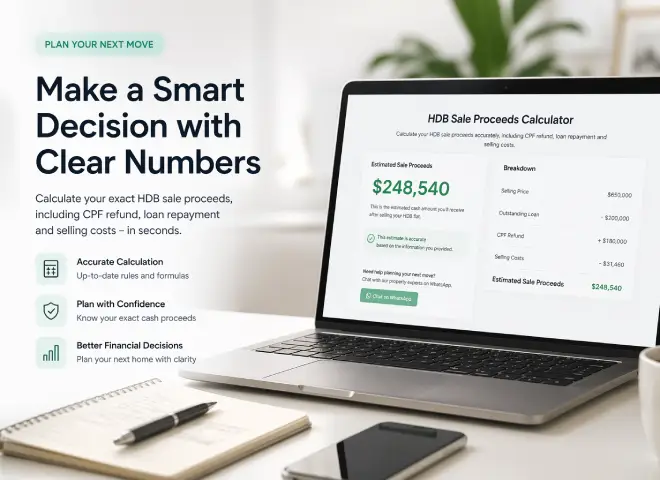

You can use the CPF housing usage calculator to estimate the amount of CPF savings that you can use.

Yes. Your CPF savings across your Retirement Account (RA), Special Account (SA), and Ordinary Account (OA) can be used to meet the Basic Retirement Sum (BRS).

Once the BRS is set aside, you may be allowed to use any excess CPF savings for housing, subject to CPF rules and limits.

If you sell your property below its market value, you must still refund the principal CPF amount used plus accrued interest. If you sell at market value but the proceeds are insufficient to cover the refund, you generally do not need to top up the shortfall in cash.

Yes. The Contra Payment Facility allows you to use the sale proceeds and CPF refunds from your current flat to offset the purchase price of your next HDB flat, reducing cash outlay or mortgage loan.

CPF math can be tricky. Avoid costly mistakes and cash shortfalls with a personalized financial assessment from our friendly agent.

No-obligation discussion • Get professional guidance

© 2026 - All rights reserved, Home123.sg