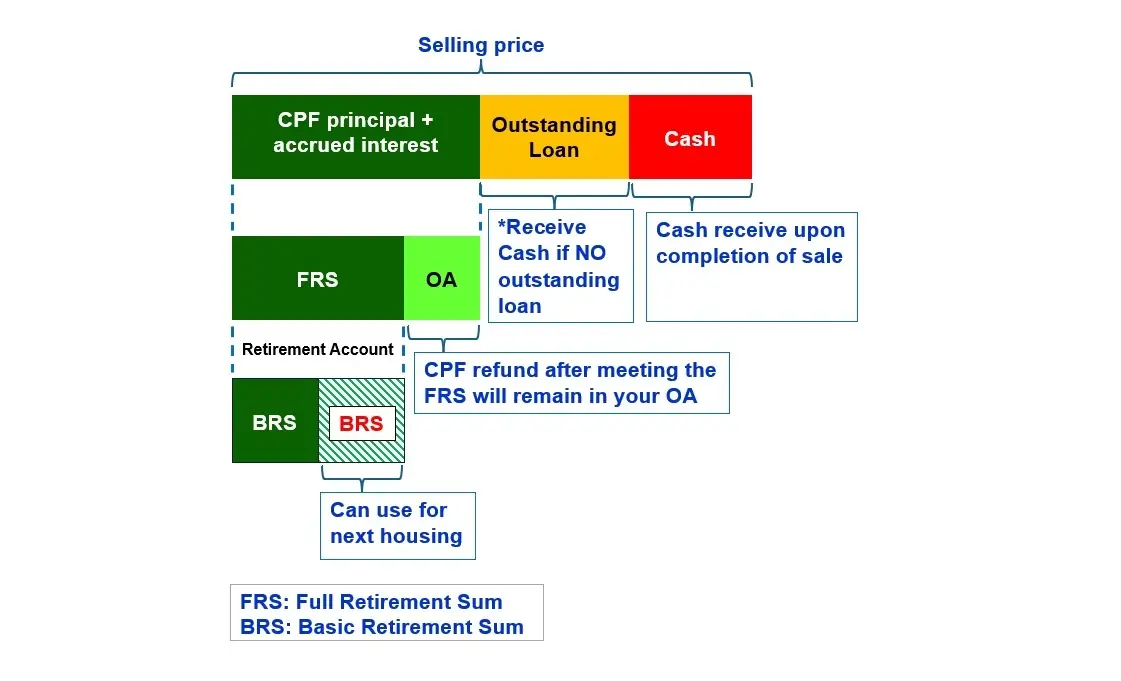

If you are planning to sell your HDB flat after age 55, it’s important to understand how your CPF savings, Retirement Account (RA), and cash proceeds are affected.

Many homeowners are surprised that they may not receive the full sale proceeds in cash — because CPF rules will apply first.

This infographic illustrates what happens when you sell your HDB flat after age 55.

When you sell your HDB flat after age 55, your sale proceeds are used in the following order:

You cannot proceed without clearing the loan

You must refund:

This amount goes back into your CPF accounts (mainly OA, then RA if needed)

If your Retirement Account (RA) is below the required amount:

CPF funds from the refund will be used to top up your RA

If your Retirement Account (RA) already meets the required retirement sum, no additional top-up is needed, and more of your sale proceeds can be received in cash.

After deducting:

The remaining balance is paid to you in Cash

| Item | Amount |

|---|---|

| Selling price | $700,000 |

| Outstanding mortgage | $150,000 |

| CPF used + interest | $300,000 |

| Cash proceeds | $250,000 |

Even after understanding CPF refunds and loan repayment, many sellers are surprised that their actual cash in hand is still lower than expected.

This is because of additional costs and financial commitments that are often overlooked:

If you plan to buy another property after selling your HDB flat, you will need to set aside cash for:

Many sellers underestimate how much they pay in selling expenses, especially agent commission.

Typical agent commission in Singapore: Around 2% of the selling price

If you sell your HDB flat with a 0.5% commission structure:

When CPF refunds and loan repayment already reduce your proceeds, keeping your selling costs low becomes even more important.

Choosing a lower commission structure can make a significant difference to your final cash in hand.

Most HDB sellers over 55 are surprised by how much their cash proceeds are reduced after CPF refunds, loan repayment, and other costs.

Don’t guess — get a clear breakdown before you sell.

We’ll help you understand:

Click below to get a personalised breakdown of your expected cash proceeds:

Get My Free Cash Proceeds Breakdown© 2026 - All rights reserved, Home123.sg